After a challenging 2025, China’s panel furniture machinery sector faces a pivotal year.

Here’s how leading manufacturers are positioning for recovery and international growth.

Industry Landscape: Pressure in the Domestic Market and New Opportunities Abroad

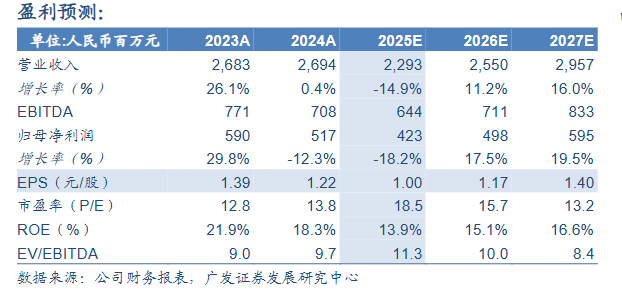

The woodworking machinery industry entered 2026 grappling with sobering realities. Hongya CNC, China’s market leader in panel furniture equipment manufacturing, reported revenue declined 14.9% year over year in 2025—a figure that signals broader industry challenges rather than isolated company struggles.

Yet within these headwinds lie distinct opportunities. Hongya’s export revenue grew 6.12% to 425 million yuan, reaching 34.4% of total revenue. This divergence between domestic contraction and international expansion reveals a strategic pivot reshaping China’s woodworking machinery sector: manufacturers who adapt to four emerging trends are well positioned for substantial growth, while those clinging to traditional domestic models face continued pressure.

Based on market analysis, government policy signals, and operational data from leading manufacturers, four trends will define competitive positioning in 2026 and beyond.

Market Context: Understanding the 2025 Downturn

China’s demand for woodworking machinery closely tracks furniture manufacturing activity, which in turn closely tracks residential construction completions.

The 2025 decline stemmed primarily from a contraction in the real estate sector—a cyclical pattern that affected all downstream manufacturing equipment.

However, leading indicators suggest inflexion points:

Year-over-year residential construction completion declines narrowed throughout 2025

Major furniture manufacturers like Tubabao saw quarterly revenue improvements, turning positive in Q3 2025

Hongya CNC’s high-margin businesses—CNC drilling, panel sawing, automated material handling, and spare parts—demonstrated resilience with gross margins rising despite market pressures.

Shanghai’s “Seven Measures” property market stimulus, released in late 2025, exemplifies policy interventions now proliferating across major Chinese cities. These initiatives aim to arrest real estate decline and, consequently, stabilise furniture manufacturing demand.

The critical question for woodworking machinery manufacturers: Which strategic moves capitalise on recovery while building resilience against future cycles? The four trends below provide directional clarity.

Trend 1: Government Infrastructure Investment Driving Domestic Demand Recovery

China’s 2025 Government Work Report outlined substantial capital deployment:

1.3 trillion yuan in ultra-long-term special treasury bonds (increase of 300 billion yuan)

4.4 trillion yuan in local government special bonds (increase of 500 billion yuan)

This capital influx funds infrastructure projects that generate downstream effects: new public buildings require furniture, renovation projects demand updated fixtures, and government facility upgrades create procurement cycles for panel furniture manufacturers.

The Equipment Replacement Cycle Convergence

Compounding government stimulus effects, the industry approaches a natural replacement cycle. Woodworking machinery typically operates 8-10 years before requiring replacement or substantial upgrading. Equipment purchased during the 2014-2016 expansion period now reaches end-of-service life.

This timing creates dual demand, drivers:

Capacity Expansion:

Government spending stimulates new furniture demand, requiring production capacity additions

Technology Upgrading:

Manufacturers replace ageing equipment with intelligent, automated systems offering better efficiency and lower labour requirements

Early indicators support recovery momentum. Sales of sanders and automated material handling equipment—both leading indicators for furniture manufacturing capacity—showed consistent month-over-month growth entering 2026, suggesting manufacturers are investing ahead of anticipated demand increases.

Implications for Equipment Manufacturers

Manufacturers positioned to benefit most:

Emphasise automation and intelligent features that justify premium pricing over simple replacement

Develop government procurement expertise and certifications required for public project

bidsOffer favourable financing terms that align with customers’ capital planning cycles

Trend 2: International Market Diversification and Emerging Economy Penetration

While Chinese manufacturers previously concentrated on domestic sales supplemented by exports to developed markets, 2026 marks a strategic reorientation toward systematic international expansion, particularly in emerging economies.

The Emerging Market Opportunity

Rapid industrialisation in Latin America, India, Southeast Asia, Africa, and parts of the Middle East is driving sustained capacity expansions in furniture manufacturing. These regions share several characteristics that favour Chinese woodworking machinery:

Price Sensitivity:

Chinese equipment costs 40-60% less than European alternatives while delivering comparable functionality for most furniture manufacturing applications

Service Requirements:

Manufacturers value responsive technical support and rapid parts availability—areas where Chinese suppliers often outperform distant European competitors

Infrastructure Gaps:

Nations building furniture manufacturing sectors from limited bases require complete production lines rather than individual speciality machines

According to industry analysis, international demand recovery accelerated through 2025 as global economic conditions stabilised. Furniture companies in emerging markets increased infrastructure investment, driving demand for woodworking machinery.

Visiting Southeast Asian countries

Navigating Trade Complexity

International expansion faces headwinds from resurging trade protectionism. Tariffs, local content requirements, and preferential treatment for regional suppliers create barriers in certain markets. However, these challenges affect all international suppliers, not exclusively Chinese manufacturers.

Successful international strategies address trade barriers through:

Regional Assembly Operations:

Establishing final assembly facilities in target markets to satisfy local content requirements while maintaining core component manufacturing in China

Strategic Partnerships:

Collaborating with established local distributors who understand regulatory environments and customer preferences

Certification Investments:

Obtaining international safety and quality certifications (CE marking, ISO standards) that facilitate market entry

The international market presents complexity but represents the primary growth vector for Chinese manufacturers as the domestic market matures. Companies systematically building international capabilities now position themselves advantageously for the next decade.

Trend 3: Used Equipment Exports Creating Secondary Revenue Streams

An unexpected opportunity emerged from China’s massive installed machinery base: used equipment exports now constitute a substantial market segment with distinct growth dynamics from new machinery sales.

Market Scale and Trajectory

Lunjiao, Shunde District, Foshan—China’s woodworking machinery manufacturing hub—hosts the world’s largest concentration of used equipment, with inventory exceeding 9 million units. Market projections estimate that this secondary market will reach 150 billion yuan by 2026.

The 2024 milestone: used sanding machine exports surpassed domestic new machine sales for the first time, signalling the industry’s entry into what analysts term the “export of existing stock” era.

Supply Drivers

Multiple factors generate a steady supply of used equipment:

Replacement Cycles:

The 8-10 year equipment lifecycle creates continuous turnover as manufacturers upgrade to newer technology

Environmental Regulations:

Emission standard upgrades and environmental compliance requirements accelerate the replacement of older equipment

Technology Migration:

Transition to intelligent, automated systems renders conventional machinery functionally obsolete for advanced manufacturers, even when mechanically sound

Demand Alignment

Used equipment demand concentrates in markets exhibiting specific characteristics:

Southeast Asia and the Middle East: Accelerated industrialisation phases with significant infrastructure gaps requiring cost-effective equipment solutions

Small-to-Medium Manufacturers: Operations prioritising capital efficiency over the latest technology, particularly in price-sensitive markets

Specialised Applications: Niche manufacturing processes where proven, reliable equipment suffices despite technological age

The price differential drives adoption: Chinese used machinery costs 60-75% less than equivalent new European equipment while offering 70-80% of functional lifespan—a compelling value proposition for capital-constrained buyers.

This trend creates opportunities for manufacturers to develop used equipment certification, refurbishment, and export services as complementary business lines alongside new machinery sales.

Trend 4: Intelligent Manufacturing Transformation Reshaping Competitive Dynamics

The most profound industry shift involves technology integration, fundamentally altering what “woodworking machinery” means. Leading manufacturers transition from selling mechanical equipment to providing intelligent manufacturing systems.

Technology Integration Drivers

Several technology streams converge in woodworking machinery:

Electrification:

Replacing hydraulic and pneumatic systems with electric drives improves energy efficiency by 25-35% while reducing maintenance requirements

Artificial Intelligence:

Machine vision systems for quality inspection, predictive maintenance algorithms anticipating component failures, and adaptive control adjusting operations based on material variations

Industrial Internet of Things:

5G connectivity enabling real-time production monitoring, remote diagnostics, and integration with broader factory management systems

Robotics Integration:

Automated material handling, robotic loading/unloading, and collaborative robots working alongside human operators

China’s “Dual Carbon” policy (carbon peak by 2030, carbon neutrality by 2060) accelerates the adoption of electrification, as electric systems reduce both energy consumption and direct emissions compared to traditional power systems.

Competitive Separation

Intelligent manufacturing capability creates widening performance gaps between industry leaders and followers. Hongya CNC’s experience illustrates this dynamic:

Traditional core businesses (basic panel processing) saw revenue share decline from 88.9% (2020) to 80.9% (2025)

Advanced systems (CNC drilling, automated material handling, intelligent control) maintained margins and grew market share despite overall industry contraction

This pattern suggests market bifurcation: commodity mechanical equipment faces price competition and margin pressure, while intelligent systems command premiums based on productivity improvements and operational cost reductions they enable.

International Standardization Opportunities

As Chinese manufacturers develop intelligent manufacturing capabilities, they gain the opportunity to influence international standards rather than merely comply with them. Leading companies promote “green intelligent manufacturing” specifications in international markets, positioning Chinese technology frameworks as viable alternatives to European or American standards.

This standard leadership carries long-term competitive value: equipment designed to Chinese intelligent manufacturing specifications creates ecosystem lock-in effects, as factories standardising on these platforms favour additional Chinese equipment for compatibility.

Strategic Implications: Navigating 2026 and Beyond

The trajectory of the woodworking machinery industry in 2026 depends substantially on how manufacturers respond to these four trends. Success requires moving beyond reactive adjustments toward a proactive strategy:

Domestic Market Recovery:

Government infrastructure spending and equipment replacement cycles create near-term domestic opportunities. Manufacturers should position for this recovery while recognizing that it offers only temporary relief rather than sustained growth—Chinese furniture manufacturing capacity ultimately exceeds domestic demand, necessitating an export orientation.

International Expansion:

Emerging markets represent the primary long-term growth vector. Systematic international capability building—certifications, service networks, regional partnerships—requires multi-year investment but determines competitive positioning through the next decade. Companies delaying international development risk permanent market-share loss to competitors who are establishing footholds now.

Technology Leadership:

Intelligent manufacturing transformation separates commodity suppliers from technology leaders. This gap will widen as AI, robotics, and IoT integration become baseline customer expectations rather than premium features. Manufacturers treating automation as optional face margin compression and market irrelevance.

Market Diversification:

Used equipment exports and services represent underutilized revenue opportunities. Developing refurbishment capabilities, quality certification programs, and emerging-market distribution channels creates business-line diversification, reducing dependence on new-equipment sales cycles.

The companies thriving through 2026 and beyond will be those recognizing these trends as interconnected rather than isolated: intelligent manufacturing capabilities enable premium positioning in international markets; government-stimulated domestic recovery provides capital for international expansion investments; and used equipment businesses fund technology R&D while serving price-sensitive emerging markets.

The fundamental question facing Chinese woodworking machinery manufacturers isn’t whether to adapt—market forces ensure adaptation or exit. The question is whether adaptation occurs reactively, under competitive pressure and diminished resources, or proactively, from positions of strength with strategic clarity.

2026 presents a window where policy support, replacement cycles, and international demand recovery align favourably. Manufacturers leveraging this convergence to build technological leadership and international presence position themselves for sustained success. Those viewing current conditions as temporary challenges to weather rather than strategic inflexion points to exploit risk, find themselves marginalized as the industry reshapes around them.

—

About LinkYou Machinery

LinkYou Machinery Manufacturing, headquartered in Lunjiao, Shunde, Foshan, specializes in intelligent woodworking equipment for furniture production. With 20+ years of industry experience, 200+ patents, including 70 invention patents, and 130+ international projects across 50+ countries, LinkYou provides comprehensive solutions from CNC panel processing to fully automated production lines. The company’s R&D focus on robotics integration, AI-powered quality control, and IoT-enabled production monitoring positions LinkYou at the forefront of China’s intelligent manufacturing transformation.

Contact:

- No.2 seconde floor ,Yingjing center Dingzi Rd ,Licuang,Lunjiao,Shunde,Foshan ,Guangdong,Chinashunde

- fengyue@163.com

- +86 13702626203

- Jelly Guan